How to read your credit card statement (and get rewarded)

Plus 3 simple rules to get more out of your credit card.

Credit cards can bring you a lot of freedom — turning your dreams into reality. No matter what your goals, they can help get you there. Take a much-needed vacation, furnish your new home, pay for tuition, start your new business venture or achieve any of life’s activities in between.

Using your card is the easy part. But it’s important to know how to read your credit card statement so you stay in control of your finances. If you don’t know what’s on your statement, you could pay more than you originally planned.

What should I review on my credit card statement?

If you’ve never read through your full credit card statement, it can be overwhelming at first. But don’t be intimidated — it’s easy to learn the key terms, and that knowledge could save you a lot of money.

Credit limit and available credit

These two terms refer to the maximum amount you are allowed to borrow on your credit card. The credit limit is the total amount you can borrow or “put on” your credit card at any one time. Available credit tells you how much room you have left to borrow (the difference between your credit limit and current balance).

Minimum payment due

Credit card companies will require you to pay at least $10 or 3% (whichever amount is greater) toward your balance owing each month. If you miss your minimum payment, you will likely be charged a penalty of $25 to $50. This penalty will be added to your balance, and interest can be applied to the penalty.

In addition, if you don’t make your minimum payment, your credit score could be lowered. With credit scores, lower is a bad thing, so you want to increase it as much as possible. On the other hand, by paying your minimum payment promptly every month, you’ll be improving your credit rating.

Account summary

The account summary is likely to be the largest section of your credit card statement. In addition to information about your previous balance, last month’s payment and your new balance owing, you’ll find a list of all the charges made on your credit card. This includes any time that you used your credit card to take out money (commonly called a “cash advance”).

Scan through this list each month and double check that you weren’t improperly charged for any items. A quick look can also help you track your spending.

Authorized vs. posted transactions

There are two types of transactions that can show up on your credit cards statement — authorized and posted. The difference is all about timing.

When you make a credit card purchase at a store or online, that charge is “authorized” but still needs to be settled by the store or service provider. Settling the charge with the credit card company could take up to five days, so during that time you’ll see the charge listed as “authorized” on your credit card statement. Note that authorized transactions aren’t included in your balance.

Once the store or service provider completes the work on their side, the credit card company will charge your card and the authorized transactions will move to the “posted” transactions section. Those posted transactions will be added to your balance owing.

Interest rates

This term is much more important than many people expect, so it’s worth spending a little more time to understand.

The interest rate is the percentage that the credit card company will charge you for any balance owing on your credit card statement. If you keep your balance at zero, you won’t have to pay any interest. The interest rate can also be referred to as APR, which stand for “annual percentage rate.”

Most Canadian credit cards charge between 12 to 20% annual interest. The lower this rate, the better in most cases — so it’s advisable to stay away from store-specific cards that climb higher.

As an example, if you have a 20% APR and a steady balance of $100 on your credit card for one full year, you’d owe the credit card company an additional $20 in interest charges. This $20 is the “price” of borrowing the initial one hundred dollars.

Daily interest rates can also come into play when you have a balance owing on your card. To calculate your daily interest rate, simply divide your yearly interest rate (or APR) by 365. For example:

- Let’s say your credit card has an interest rate of 19.99%

- 19.99% divided by 365 = 0.055

- Your daily interest rate would be roughly 0.055%

To further explain how this daily rate could impact you, let’s say your credit card statement arrives and shows that your current balance owing is $5,000. If you’re only able to pay $4,000 before the payment due date, you will owe another $1,000. Based on your 0.055% daily interest rate, you will have to pay roughly 55 cents for every day that you don’t pay your final $1,000.

This money might seem like small change, but it can add up in a hurry. Especially if you keep adding to the amount you’re not paying off each month.

Annual fee

Some cards charge an annual fee in exchange for premium rewards like travel, gifts and cash back, which can be a great way to save on those types of purchases. Fees generally range from $20 to $120 per year, and in some cases, you could pay much higher for premium cards.

Other cards have no annual fee at all, but they may not offer many (or any) incentives.

Rewards

There is an upside to higher rate credit cards: Rewards!

This can be the most fun part of owning a credit card, as you can earn incentives for using your card regularly. These rewards can include travel points for flights and vacations, free movie tickets, must-have electronics and even “cash back” on purchases.

For example, by using your credit card for daily expenses like gas and groceries, plus large purchases like new home furnishings, you can rack up a lot of points and exchange them for an all-inclusive trip to Mexico. The type of rewards available are dependent upon the card you sign up for.

This can be a powerful bonus if you use your credit card wisely. If you don’t carry a balance on your card because you make regular and prompt payments (for example, you use your card to purchase groceries and gas, then transfer funds from your chequing account that same week to cover those amounts on your credit card), then you can really profit from a card’s rewards program.

Make a habit of regularly transferring funds to your card and paying off those charges. Otherwise, you’ll be paying more for interest than you’ll receive back on rewards. And as a word of caution, never try to collect credit card rewards at the expense of your overall financial health.

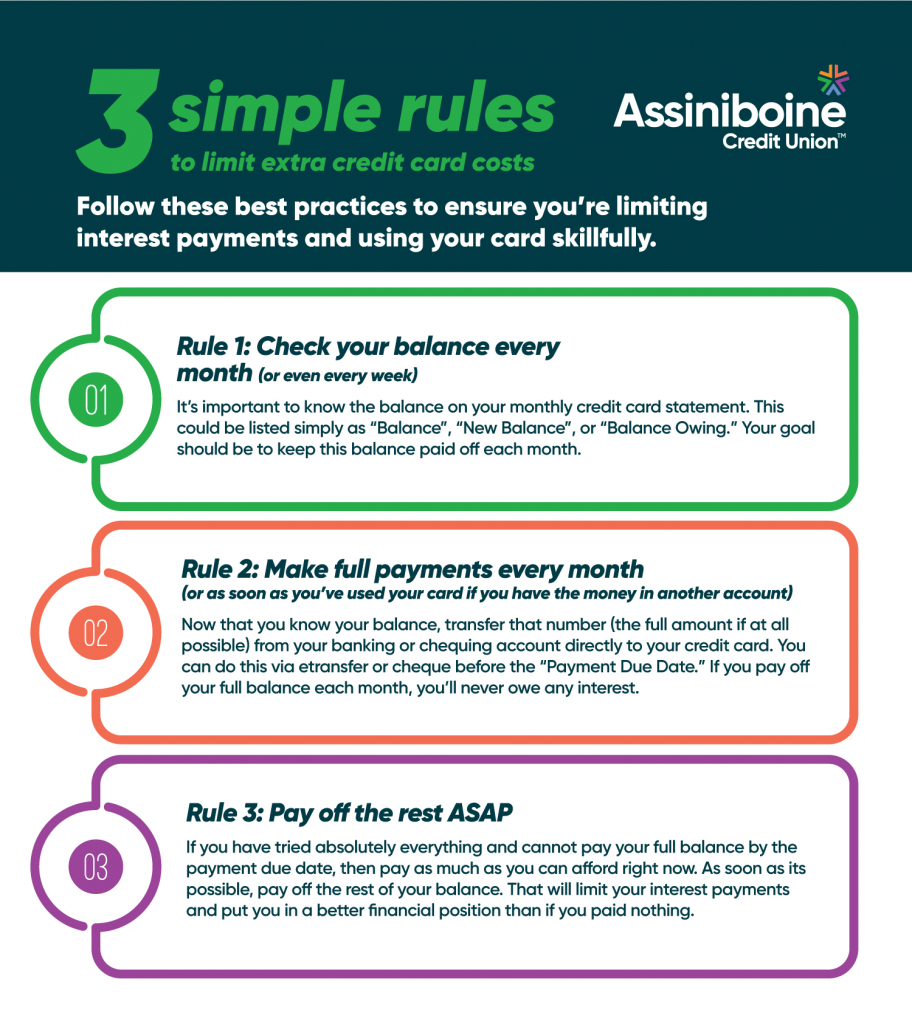

Download this graphic: 3 simple rules to limit extra credit card costs

3 simple rules to limit extra costs

Now that you know what to look for in your credit card statement, follow these best practices to ensure you’re limiting interest payments and using your card skillfully.

Rule 1: Check your balance every month (or even every week)

It’s important to know the balance on your monthly credit card statement. This could be listed simply as “Balance”, “New Balance”, or “Balance Owing.” Your goal should be to keep this balance paid off each month.

Rule 2: Make full payments every month (or as soon as you’ve used your card if you have the money in another account)

Now that you know your balance, transfer that number (the full amount if at all possible) from your banking or chequing account directly to your credit card. You can do this via etransfer or cheque before the “Payment Due Date.” If you pay off your full balance each month, you’ll never owe any interest.

Rule 3: Pay off the rest ASAP

If you have tried absolutely everything and cannot pay your full balance by the payment due date, then pay as much as you can afford right now. As soon as its possible, pay off the rest of your balance. That will limit your interest payments and put you in a better financial position than if you paid nothing.

Once you know where to look on your credit cards statement and understand which numbers matter most, managing your finances can be a simple monthly routine. Keep an eye on your spending habits, your monthly budget and then follow the three simple rules to limit your extra interest costs.

You’ll feel completely in control of your credit card, and just might be able to take that vacation of your dreams.

Up Next

Celebrating the 10th anniversary of student-run credit union

Just over 10 years ago, a survey circulated at Winnipeg’s Technical Vocational High School. The results showed that students at the school, commonly known as Tec Voc, felt short-changed—they were…

Kilter Brewing Co. serves up craft beer and community connection in St. Boniface

Deep in the heart of St. Boniface, Kilter Brewing Company is a hidden treasure—an oasis for Winnipeggers to escape their day-to-day routines, enjoy craft beer and connect with their community….

How to use a mortgage calculator to budget better

Learn how to use ACU’s mortgage calculator to figure out how much mortgage you can afford, and what budget you should set before you start house hunting. A mortgage lender…